FRIDAY AGGREGATE: Smart Meters; Core Gas Deliveries; RPS Milestones

This week’s filings reflect growing conflicts between lifecycle infrastructure replacement, policy-driven procurement targets, and the physical limit of electric and gas systems.

SMART METERS

SDG&E filed an application seeking CPUC approval to replace its aging Smart Meter 1.0 advanced metering infrastructure with a new Smart Meter 2.0 platform, citing widespread device failures, approaching end-of-life between 2026–2028, and growing risks to billing accuracy, outage management, cybersecurity, and customer service.

The proposal requests authority to recover approximately $825 million in costs incurred from 2024 through 2031 for system design, foundational and next-generation technology, and mass deployment of new electric meters and gas modules, while reusing portions of existing infrastructure where feasible to limit customer impacts.

SDG&E also seeks approval of a new two-way, interest-bearing Advanced Metering Infrastructure Balancing Account to track and reconcile authorized revenues, and requests an expedited schedule so deployment can begin in 2027 before failure rates outpace workforce capacity and vendor support ends. SDG&E argues that delaying the transition would materially increase program costs and operational risk, and that Smart Meter 2.0 is necessary to preserve core functionality while supporting future grid modernization and customer-facing capabilities.

Protests/responses are due January 21.

INSTANT ANALYSIS: SDG&E’s Smart Meter 2.0 application is a ratepayer-funded infrastructure replacement case driven by hard end-of-life risk rather than feature expansion. Smart Meter 1.0 meters that were deployed in 2009–2011 are failing at accelerating rates, vendor support is winding down, and workforce capacity to manage failures is projected to be exceeded by 2026. SDG&E seeks expedited approval to recover $825 million in electric and gas rates via a new balancing account, arguing that delay would both degrade billing accuracy and outage visibility and increase total program costs. The core regulatory question is not whether replacement is needed (the Commission previously acknowledged Smart Meter 1.0 would require full replacement) but whether the scope, pacing, and cost controls of the Smart Meter 2.0 rollout are sufficiently disciplined to justify full rate recovery on an accelerated schedule.

NATURAL GAS RATES

SoCalGas/SDG&E filed an advice letter (AL 6573-G, available here), which provides their biannual report on cost impacts to core customers arising from the requirement, adopted in a 2019 decision (D.19-08-002), that core gas deliveries be balanced to estimated actual consumption rather than forecasts.

Covering the period from June 1 through November 30, 2025, the filing reports that SoCalGas’s system operator declared a total of 118 Operational Flow Orders (almost entirely High OFOs, with no Low OFOs until November) and no noncompliance charges incurred by Gas Acquisition during the reporting period.

The utilities describe mitigation measures taken by Gas Acquisition to manage OFO exposure, including the continued use and periodic adjustment of daily Usage Guidelines to respond to uncertainty in core demand and the achievement of required storage injection targets. While the utilities acknowledge that these mitigation actions may have limited opportunities to reduce procurement costs relative to benchmarks, they state that any such impacts cannot be reliably quantified without significant assumptions.

INSTANT ANALYSIS: This filing shows that, despite a heavy concentration of High OFO days during summer and fall 2025, SoCalGas’s Gas Acquisition operations avoided noncompliance charges by relying on conservative balancing practices and internal usage guidelines. For core customers, the immediate takeaway is stability rather than savings: mitigation actions reduced exposure to penalties but may have constrained opportunities to lower procurement costs, highlighting a continued tradeoff between operational compliance and cost optimization under the post-D.19-08-002 balancing regime.

RPS PROGRAM

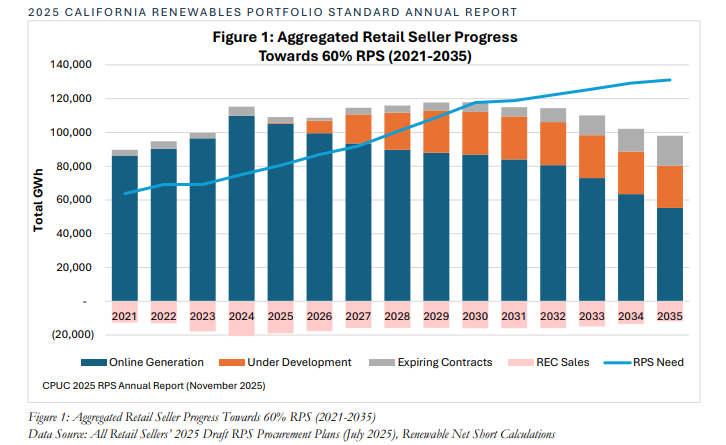

The CPUC published its 2025 California Renewables Portfolio Standard Annual Report. The report finds that California’s electricity retail sellers are broadly on track to meet the state’s statutory requirement to supply 60% renewable electricity by 2030, with most entities meeting or exceeding the interim, non-binding 44% renewable target for 2024.

Community Choice Aggregators and Electric Service Providers generally exceeded annual targets, while investor-owned utilities and Small and Multi-Jurisdictional Utilities relied more heavily on previously banked Renewable Energy Credits to demonstrate compliance for the 2021–2024 compliance period.

| IOU | Percent |

|---|---|

| Pacific Gas and Electric | 28% |

| Southern California Edison | 38% |

| San Diego Gas & Electric | 45% |

Over the past decade, average RPS contract prices have declined steadily due to falling wind and solar costs, though prices rose in 2024 amid end-of-period procurement pressure, supply-chain uncertainty, and inflation concerns. Since 2020, more than 24 gigawatts of new renewable generation and storage have interconnected to the CAISO grid. However, transmission delays remain a serious constraint.

The report’s Senate Bill 1174 assessment shows that a majority of PG&E and SCE transmission projects are delayed, placing about 13 gigawatts of renewable and storage resources at risk of delayed operation. In response, CPUC staff highlight ongoing coordination with the CAISO and other agencies to address permitting, materials, and project-sequencing challenges, while emphasizing that Integrated Resource Planning will increasingly guide renewable procurement.

INSTANT ANALYSIS: The 2025 RPS Annual Report confirms that California is meeting near-term renewable targets largely through portfolio management and banked RECs rather than sustained new-build momentum. While headline compliance remains intact across most retail sellers, rising 2024 contract prices and growing reliance on excess procurement point to tightening conditions at the margin. The most consequential risk sits outside procurement itself: persistent transmission delays now place more than 13 GW of renewable and storage resources at risk, directly threatening the pace and timing of future RPS delivery. Absent accelerated transmission resolution and interconnection reform, RPS compliance increasingly becomes an accounting exercise rather than a physical system outcome, which will compound as IRP-driven procurement ramps and the state pushes toward Senate Bill 100 targets.

INTERCONNECTION/LARGE LOADS

PG&E filed an advice letter seeking CPUC approval of a non-standard Electric Rules 2, 15, and 16 agreement to interconnect a new Google LLC facility in San Jose with a forecasted full-build demand of 250 megawatts at the transmission level.

To serve the load, PG&E proposes an arrangement under which Google would design, construct, and initially fund a new 230 kilovolt gas-insulated switching station. The station would have a breaker-and-a-half configuration, along with associated underground transmission service lines connecting to a PG&E-owned switching station, with ownership of certain facilities transferred to PG&E upon completion.

The estimated cost of the interconnection facilities ranges from $64 million to $137 million, exclusive of income tax gross-up, with an anticipated in-service date of December 2028. PG&E frames the agreement as protective of existing ratepayers by relying on:

- Actual-cost billing;

- Binding cost estimates for applicant-built facilities;

- Refund limits tied to the lower of actual or estimated costs; and

- Explicit provisions requiring Google to bear unreimbursed special-facility costs and any costs incurred if the project is terminated.

The advice letter also identifies preliminary cost-recovery venues, indicating that facilities integrated into the CAISO-controlled transmission network are likely to be recovered through FERC-jurisdictional transmission rates, while certain service lines and metering equipment would remain CPUC-jurisdictional.

Protests are due January 7.

MICROGRIDS

PG&E filed an advice letter providing its quarterly update on the Microgrid Incentive Program, covering program and project activity through September 30, 2025.

The report describes PG&E’s progress administering its authorized $79.2 million Microgrid Incentive Program budget, which is intended to support clean community microgrids that serve critical facilities and disadvantaged or vulnerable communities impacted by grid outages.

As of the reporting period, program activity remains concentrated in early stages, with extensive community and developer engagement underway: 47 projects in Tranche 1 and 56 projects in Tranche 2 are in Stage 1 consultation, while 22 Tranche 1 projects have advanced into Stage 2 application review.

No projects have progressed to the construction or operational stages, and no incentive award payments have been made. Spending to date consists primarily of administration costs and a limited amount of capital spending associated with the Redwood Coast Airport microgrid under the separate Community Microgrid Enablement Program framework, with no accruals or outstanding contractual commitments reported as of September 30.

PG&E states that forecasting remains constrained until project awards are finalized, and reports no program issues requiring mitigation at this time.

INSTANT ANALYSIS: This filing is procedural but revealing: more than a year into PG&E’s Microgrid Incentive Program, activity remains clustered in consultation and application review, with no projects reaching construction or operation and no incentive awards issued. For market participants, the near-term takeaway is straightforward: Microgrid Incentive Program dollars remain largely uncommitted, timelines are extending, and tangible resiliency gains are arriving later than statutory or policy narratives suggest. Early-stage engagement and project readiness therefore matter more than any assumption of shovel-ready deployment.

MOSS LANDING

The Western Electricity Coordinating Council has released a report analyzing the January 16 fire that destroyed Phase 1 of the Moss Landing battery energy storage system.

- The report uses the incident to highlight how early, warehouse-style Battery Energy Storage System designs (built before National Fire Protection Association 855 and large-scale UL 9540A fire testing) carry elevated risks compared to modern systems. The fire occurred during a high state-of-charge capacity test, a condition strongly associated with thermal runaway; it overwhelmed suppression systems, prompted evacuations, and ultimately resulted in a total loss of the Phase 1 facility, with a later re-ignition tied to residual damage.

- The report situates Moss Landing within a broader pattern of BESS fires, emphasizing thermal runaway and high State of Charge as primary risk drivers, the limits of traditional indoor suppression strategies, and the industry’s shift toward containerized designs, updated codes, validated fire testing, and safer operating practices.

INSTANT ANALYSIS: The WECC’s report frames the January 2025 loss as a legacy-design problem rather than a repudiation of grid storage. The report reinforces that once thermal runaway begins, suppression in dense indoor installations may not prevent propagation. Modern safety practice has therefore shifted toward containerized designs, validated fire testing, tighter State of Charge limits, and more disciplined operating and emergency-response protocols (particularly for older facilities still operating outside today’s design standards).