CAISO Draft Plan: Congestion Surge Forces $7 Billion Transmission Buildout to Serve Load Growth

The CAISO published its draft 2025–2026 Transmission Plan, which identifies 38 transmission projects totaling $7 billion over the next decade. These projects combine new infrastructure with upgrades to existing lines, plus the targeted use of grid-enhancing technologies to expand capacity at lower cost.

The draft plan reflects a shift in California's transmission needs. Earlier planning cycles focused on accessing remote renewable resources. This one is driven by load growth (electrification, manufacturing, and data centers), with reliability needs now outweighing policy-driven renewables expansion.

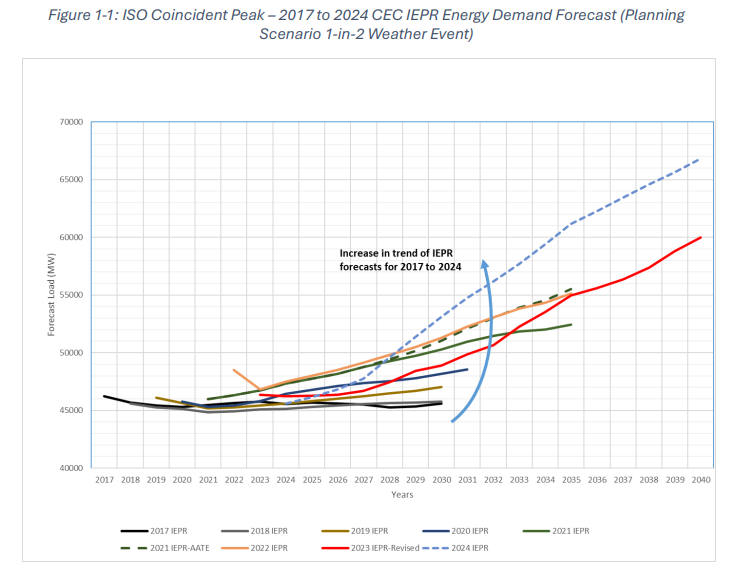

State forecasts underpinning the plan show load growth of 15 GW by 2035 and 20 GW by 2040, with installed resource capacity needing to increase by more than 74 GW and 107 GW, respectively. This will force a coordinated expansion of generation and transmission at a scale California has not previously planned for.

Congestion is the central cost driver. Path 15 congestion forecasts have increased tenfold in five years: the 2021–2022 plan projected 244 hours of congestion on the most limiting circuit by 2030. The draft plan projects 3,256 hours by 2035. The CAISO frames transmission expansion explicitly as a tradeoff: upfront infrastructure cost versus sustained high-cost dispatch that shows up in energy charges.

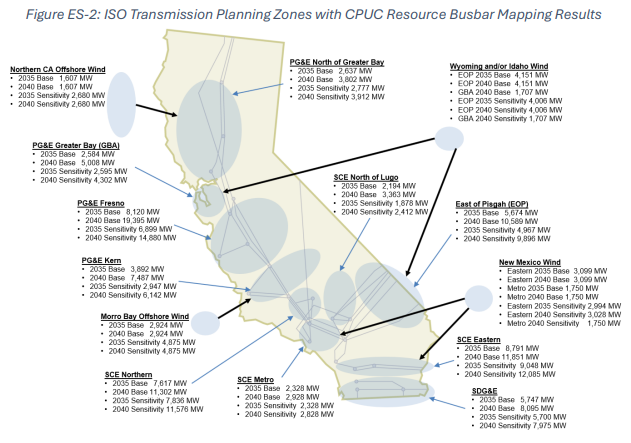

Geographically, the draft plan prioritizes the Greater Bay Area, the Central Valley, and key import corridors from the Southwest. It supports the planned buildout of 45 GW of solar, 8 GW of in-state wind, over 2 GW of geothermal, 10 GW of imported wind, and 4.5 GW of offshore wind, with battery storage co-located at generation sites and positioned near major load centers.

Key projects include:

- The Tesla–Trimble–Metcalf 230 kV corridor expansion for the south Greater Bay Area;

- The Trout Canyon–Lugo 500 kV line for East of Pisgah resources;

- Gates–Los Banos #3 500 kV series compensation for Path 15 congestion; and

- A proposed Windhub–Tesla 500 kV line to further relieve Path 15, which requires additional engineering refinement and is not expected to be recommended for approval until the next planning cycle.

Of the 38 projects, 12 include reconductoring, three of which use advanced conductors as the most cost-effective solution. The CAISO Board of Governors will consider the draft plan at a virtual meeting on May 19. Prior to that, an April 15 stakeholder call will review the draft plan and solicit feedback.

INSTANT ANALYSIS

This draft plan is load growth materializing in hard infrastructure. Data centers, electrification, and industrial demand are the primary drivers of transmission buildout, not renewables integration.

The real story is the congestion curve turning vertical. Path 15 has moved from a manageable constraint to a persistent cost driver in a single planning cycle. A tenfold increase in forecast congestion hours forces the CAISO to justify large capital deployment as near-term cost containment, not long-lead planning.

For market participants, this is a forward signal on basis risk and deliverability. Congestion will rise before these projects come online, which means localized price separation, curtailment risk in resource zones, and increasing value for assets positioned inside constrained load pockets.

WHO IS MOST AFFECTED

- Large load developers (data centers, industrials): These entities are driving the buildout and will face interconnection timelines, deliverability constraints, and cost-allocation battles. Siting decisions will determine whether they will hit delays or premium infrastructure costs.

- Investor-owned utilities (PG&E, SCE, SDG&E): The IOUs inherit execution risk. Projects flow into rate base under rising affordability pressure and scrutiny over transmission spending.

- Noncore gas and large electric customers: Transmission buildout tied to electrification raises delivered power costs, while parallel gas system underutilization drives a second layer of cost reallocation.

- Developers in constrained resource zones (Central Valley, imports, offshore wind): Deliverability is the bottleneck. Projects without firm transmission access face curtailment risk and weaker economics until upgrades are in service.

- Traders and structuring desks: The draft plan is a congestion map. Expect widening nodal spreads, more persistent basis risk, and increased value in congestion hedging around load pockets and constrained paths.

- Community Choice Aggregators and Load-Serving Entities: Transmission timing mismatches with resource buildouts increase exposure to RA compliance costs and will force more expensive local procurement.

- Ratepayers: These costs show up gradually but are real. Transmission is framed as cost avoidance via congestion relief, but near-term bills reflect layered infrastructure spend.

Transmission is no longer a background constraint. It is becoming the primary determinant of where load can land and where generation can clear.