Deep Dive: The Sempra IOUs' $5 Billion Post-Test-Year Ratemaking Gambit

On January 16, multiple parties responded to a petition for modification filed by SoCalGas/SDG&E (the Sempra Utilities) seeking changes to the post-Test-Year ratemaking mechanism adopted by the CPUC in a 2024 decision, D.24-12-074. (See CRI's coverage of the Sempra Utilities' petition here).

The Sempra Utilities claim the adopted mechanism leaves approximately $5 billion in capital-related revenue requirements unfunded over the 2025–2027 post-Test-Year period.

Opposing parties (Indicated Shippers/Environmental Defense Fund, TURN/Southern California Generation Coalition, Cal Advocates, and the Protect Our Communities Foundation) argue that the petition is procedurally improper and substantively deficient. They contend that SoCalGas/SDG&E are attempting to relitigate issues that were expressly resolved in the underlying General Rate Case, and the petition functions as an untimely application for rehearing rather than a legitimate request for modification.

- Opposing parties emphasize that Rule 16.4 (available here) and Public Utilities Code §1708 require genuinely new facts, changed circumstances, or a clear misconception of law or fact, none of which are present. In their view, an alleged “revenue shortfall” identified by the utilities arises only because the CPUC rejected the utilities’ preferred capital-driven escalation framework in favor of a uniform 3% CPI-based post-Test-Year mechanism. The latter mechanism is designed to moderate rate growth, address affordability concerns, and constrain rate-base expansion in the context of declining gas demand.

- The parties argue further that granting the petition would undermine regulatory finality and violate due-process expectations of parties to the GRC. TURN/SCGC specifically argue that retroactively modifying the post-Test-Year mechanism and adjusting previously collected revenue requirements raises retroactive ratemaking concerns, citing case law establishing that the CPUC may not retroactively increase rates previously adopted after a full hearing.

- Opposing parties defend the CPUC’s policy judgment in D.24-12-074, stressing that post-Test-Year mechanisms are not intended to guarantee full recovery of all projected capital expenditures or to replicate a test-year cost-of-service analysis. Instead, they characterize post-Test-Year ratemaking as a discretionary tool meant to provide utilities a reasonable opportunity to earn their authorized return through prudent management, while balancing ratepayer protections.

- TURN/SCGC notably concede that O&M expenses and capital expenditures do affect revenue requirements differently (their own proposal in this proceeding used a two-part mechanism) but argue the CPUC has broad discretion to fashion an appropriate post-Test-Year mechanism in each General Rate Case, or to provide no mechanism at all.

- Protect Our Communities Foundation raises additional arguments not emphasized by other opposing parties: that the utilities failed to account for billions of dollars in deferred taxes (ratepayer-provided cash available at zero cost for capital projects) when calculating their alleged "missing money." PCF also argues that capital expenditures should be trending downward given that the Pipeline Safety Enhancement Program began over 15 years ago and wildfire mitigation programs have been in place since 2019.

- Opposing parties also note that the CPUC already authorized significant Test-Year revenue increases, adopted targeted exceptions to the 3% escalation for specific capital programs, and approved memorandum accounts for gas integrity and other defined activities. In this context, they argue that the petition’s requested two-part capital mechanism would upset the careful balance struck in the decision and shift risk from shareholders to ratepayers in ways inconsistent with affordability objectives.

- Indicated Shippers/Environmental Defense Fund add that the utilities' proposed "rate smoothing" mechanism is a disguised attempt to prevent a scheduled rate decrease (resulting from the roll-off of existing memorandum account amortizations) from reaching customers' bills.

By contrast, PG&E and SCE support the petition and align with the Sempra Utilities' central argument that the CPUC's adoption of a one-part post-Test-Year mechanism rests on a misconception of how capital costs affect revenue requirements.

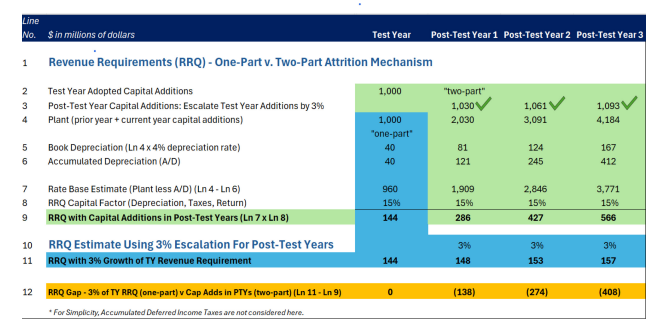

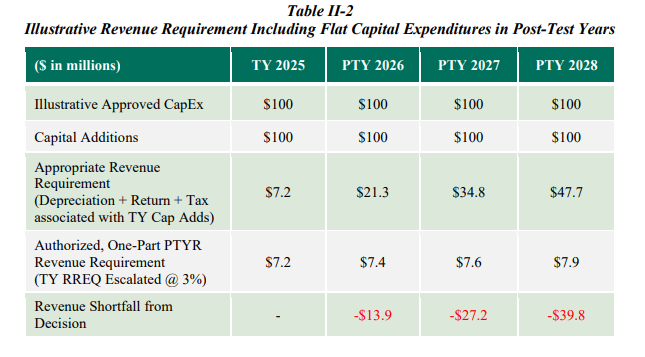

The utilities assert that capital expenditures, unlike O&M expenses, translate into revenue requirements through depreciation, return, and taxes over time, and that applying a single escalation factor to total revenue requirement materially underfunds capital additions in the post-Test Years.

Both PG&E and SCE provide illustrative tables (see below), which show that a one-part mechanism funds capital additions only for the Test Year, leaving significant revenue requirement shortfalls in each subsequent attrition year.

The utilities argue that this underfunding threatens their ability to complete Commission-approved capital projects necessary for safety, reliability, and risk mitigation, and increases the likelihood of rate volatility in future GRCs. PG&E and SCE maintain that long-standing Commission precedent supports a two-part post-Test-Year framework that separately addresses capital additions, and that modifying D.24-12-074 to adopt such an approach would better align the decision with the regulatory compact and constitutional requirements to provide utilities a fair opportunity to earn their authorized returns.

INSTANT ANALYSIS: The Sempra Utilities' petition for modification faces broad resistance from ratepayer, environmental, and public-interest parties, who argue it is an improper attempt to relitigate the post-Test-Year mechanism adopted in D.24-12-074 and fails to meet the Rule 16.4 standard for new or changed facts. These parties defend the Commission’s uniform 3% CPI-based escalation as a deliberate affordability and rate-base-control measure, warning that reopening the decision would undermine regulatory finality and raise retroactive ratemaking concerns. Support comes primarily from other utilities, who contend the one-part post-Test-Year mechanism significantly underfunds capital additions and departs from precedent. The CPUC's treatment of this issue will demonstrate how firmly it intends to hold the line on post-Test-Year moderation in the face of renewed utility pressure.